HOME | ABOUT US | MEDIA KIT | CONTACT US | INQUIRE

HOME | ABOUT US | MEDIA KIT | CONTACT US | INQUIRE

*/?>

*/?>

The quadrennial presidential popularity contest is nearly upon us. With November fast-approaching, our constituency deemed it appropriate to review the returns of the S&P 500 under the six separate iterations of political control. Is a divided government the answer to investment prosperity? Does full Republican or Democratic control of our democracy bode best?

Luckily, dependent up-on your political leanings, you can spin it however you prefer (just like any good politician). The differences were interesting, if not entirely definitive. A Republican-controlled government, for example, has produced the highest annualized returns; however, Democratic presidencies have a higher average return under all congressional makeups.

While good for political season cocktail-party chatter, the same data also concluded that no significant relationship exists between election results and subsequent market returns. Unfortunately, those same cocktail parties in all likelihood will see less-healthy debate as political polarization continues to magnify at a fevered pitch.

This mutually shared hatred for “those idiots on the other side” does not bode well for unified efforts to move our country forward. It’s too early to decipher real potential policies from the rhetoric being spewed, but this election cycle has the makings for generating outsized influence on the investment markets.

While political muckraking is nothing new, a vanguard acronym has entered the financial lexicon; NIRP, as in Negative Interest Rate Policy.

In a nutshell, central banks are now punishing regional banks, corporations, and individuals for hoarding cash. By eliminating or even creating disincentives to save, the hope is that by forcing money out of savings accounts, it can better serve the overall economy. In other words, get banks to lend more, while businesses and individuals spend more.

Results have been mixed. Interestingly, Japan is the only country that has actually started to see banking customers charged for holding checking and savings accounts. The unintended consequence has been a shortage of safes in Japan, as savers have pulled money out of traditional banks to literally keep at home.

As we have bemoaned before, the Federal Reserve and other central banks around the globe are in the midst of an incredible monetary experiment that has never been performed before. Negative interest rates are only the latest attraction of this stimulus circus.

As we have bemoaned before, the Federal Reserve and other central banks around the globe are in the midst of an incredible monetary experiment that has never been performed before. Negative interest rates are only the latest attraction of this stimulus circus.

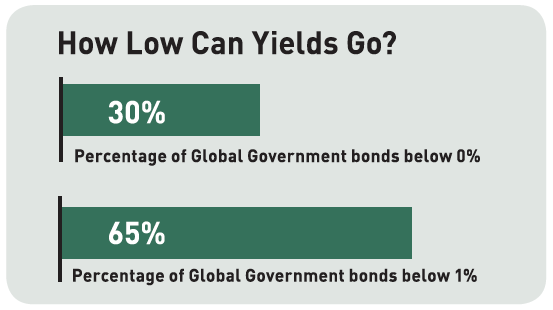

There are now five major central banks around the globe with stated negative interest-rate policies. Amazingly, 30 percent of government bonds worldwide now have negative interest rates attached to them. A full 65 percent of global government bond debt yields less than 1 percent, highlighting the challenges for savers and conservative investment strategies.

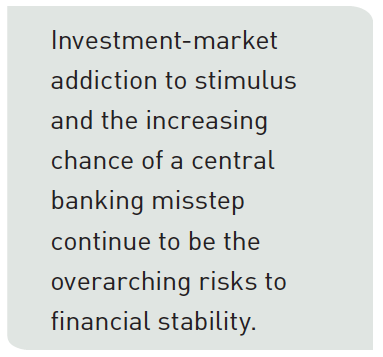

While not appearing to be a problem in either the short or mid-term, investment-market addiction to stimulus and the increasing chance of a central banking misstep continue to be the overarching risks to financial stability. Less reliance on omnipotent central banks will lead to stronger and more efficient capital markets.