HOME | ABOUT US | MEDIA KIT | CONTACT US | INQUIRE

HOME | ABOUT US | MEDIA KIT | CONTACT US | INQUIRE

The storm that has beseiged office and retail has battered commercial realty nationwide, but broker/execs say things overall are bearable in Kansas City.

Remember the grave-robbing scene from Young Frankenstein? The good doctor remarks on the filthy task, and Igor puts an optimistic spin on it: “Could be worse.”

“How?”

“Could be raining.”

(Lightning flashes, downpour begins.)

If you’re in commercial real estate sales and brokerage today, you just have to hope that no one suggests things could be worse.

Consider: On the retail side of things, the Kansas City region’s last retail outlet bearing the storied brand of the Sears, Roebuck & Co. legacy—a Sears Home & Life store in Overland Park—threw in the towel just this month by starting a liquidation sale.

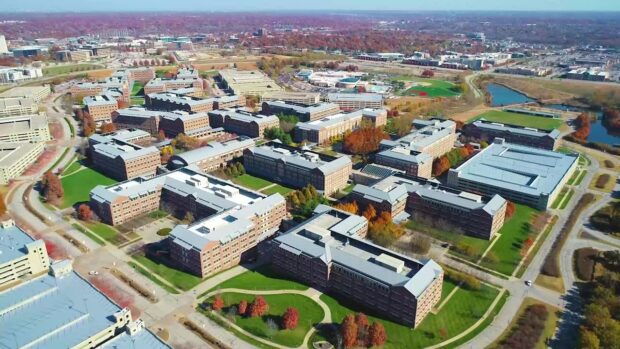

On the office side, leasing activity continued to slow nationwide, according to Jones Lang Lasalle, with vacancy rates rising and the specter of defaults arising with coming debt maturities. Leasing volume recorded a third straight quarter of slumping demand—down nearly 10 percent from the final quarter of 2020, while leasing activity was also 10.7 percent lower than the final quarter of 2022.

Not the cheeriest of news, but as Igor might have said, it could be worse. How? Well, a 20.8 percent market vacancy rate here is no picnic, but it’s better than the 29.9 and 25.4 percent rates in the Connecticut locales of Fairfield County and Hartford, Conn., the 26.8 percent in New York’s Westchester County, the 26.3 percent in Columbus, the 26 percent in Houston, the 24.6 percent rate in Minneapolis—it’s a fairly dismal list on a national scale.

One thing all of those locations have in common is that they are well above the national office vacancy rate of 18.2 percent, itself up from 16.4 percent in the final quarter of 2021.

“There’s a strange combination of things affecting office markets” nationally, says Bucky Brooks of Copaken Brooks. “Specific to office, that market is not going away, but it’s changing. Tenants are trying to get their feet set as to what that’s going to look like. What we’re seeing is many companies are considering reducing their footprint, but they still want an office and want to be in a nicer and different configuration, with more amenities in that space.”

From a broker’s point of view, he says, “That makes life more difficult; uncertainty means tenants, in most cases, are less willing to commit to a long-term lease. They’re considering how to reduce or change their space for the better, if they can. That means a shorter term in net reduction and more expensive buildouts. That makes things challenging.”

While slow, the office market is nowhere close to dead, Brooks says. Rather, “more and more, employers are really now recovering from the hybrid work model, not that it’s going away, either, but many are trying to get employees back into the office.”

According to Jones Lang Lasalle’s market assessment for the first quarter of 2023, technology has been dethroned as the top sector for office leasing activity, something to be expected following the layoffs of tens of thousands in that sector. Leasing in that sector was off more than half from its pre-pandemic levels.

Tech ceded the No. 1 spot to banking and finance for office lease deals in the quarter, accounting for 29.4 million square feet of deals.

Of course, the industrial market that caught fire in this region a decade ago continued to burn, notching a 3.1 percent vacancy rate in the quarter. And multifamily remains strong, though having backed off a bit from its peaks over the past five years.

That leaves retail, where Owen Buckley of LANE4 Property Group continues to navigate seas that turned stormy long before the pandemic showed up. But the owners of retail spaces are figuring out a response to the e-commerce explosion of the past 15 years.

Speaking just hours after Bed, Bath & Beyond became the latest big-box gladiator to fall in battle, Buckley nevertheless says, “I do think things have stabilized a bit. Online and the physical store will both be very important outlets for retail, each playing an important part. People like convenience; that never goes out of style. With most things you see in this country, no matter what it is, success seems to be based on the conveniences of something—people enjoy that experience because it saves time. Ordering online and getting products delivered to your door is something people like.”

At the same time, there are shopping experiences for which a computer is no substitute. People want to assess the look, the feel, and the style of something before they buy it. That’s hard to do from a mobile app.

“We’re social creatures, we like to interact, to touch, feel and try different things on, try different foods, so the physical part of retail will continue to be strong,” Buckley said. “We haven’t seen a lot of new construction in general over the last 10-12 years, so I think that’s helping, too. Every day, the country is getting bigger, but we haven’t built much retail,” which helps right-size the environment in a changing sector.

One important issue facing commercial realty is the way investors are assessing opportunities.

With office space, said Kerr, “I think the money is there; the question is how much pre-leasing you have to do to kick a project off. In the past, it’s been about 40 percent, but now that number may be a little higher.”

Because of bearish sentiment on offices in the lower tiers of Classes B and C, he says, there’s a flight to quality—by both investors and companies seeking space—in the newer Class A properties that are more attractive and have better amenities such as coffee bars and on-site gyms for employees.

“People gravitate to the new office space,” he said. “A lot of it because it has been a tight labor market. More owners are viewing office space as an HR tool, and companies need to be in a really nice office building if they want to attract and retain the best talent in the business. Because of that and how well Class A is doing in Kansas City, we do have available opportunities for some new offices to be built, and I think they will lease-up. I think the demand is there.”