HOME | ABOUT US | MEDIA KIT | CONTACT US | INQUIRE

HOME | ABOUT US | MEDIA KIT | CONTACT US | INQUIRE

It’s been a wild ride in U.S. bank lending over the past decade, one that in some ways is like a roller coaster—a long, steady climb to a very high peak, leading up to the onset of the Great Recession in 2007 and a massive, stomach-churning plunge through 2008, then a steady recovery, with occasional dips and surges since then.

An analysis of FDIC bulk data over that period offers some insights into how the KC banking market, in particular, has changed in just a decade—not just in the numbers of banking options available to businesses and individual consumers, but the way banks’ lending patterns have changed, as well. In short, the data tell the story of where the money is flowing.

The vast majority of regional lending activity is being managed by slightly more than three dozen banks, those with loan portfolios of at least $100 million. Those 37 banks are among the 83 based in the Kansas City metropolitan statistical area (the FDIC statistics reflect the lending figures for those banks headquartered here). Among the insights gained from crunching tens of thousands of data points for the 10-year span from 2006 to 2015:

Interesting, as well, is the changing nature of the lending game.

While there’s general consensus that the real-estate market has largely recovered from the 2008 housing crisis, real estate loans are still short of their 2006 level, totaling $21.8 billion in 2015, down 1.31 percent from 2006. That figure is still critical, because it accounts for more than half of all lending volume among those banks.

The areas for biggest lending growth may surprise anyone not employed by a bank, but not anyone familiar with the reach of this region’s agricultural economy. While the study group

included key categories like commercial and industrial loans, individual credit-card loans, construction and development loans and residential property loans, the biggest growth category entailed farmland and farm loans, up an impressive 105.1 percent.

Among those other categories:

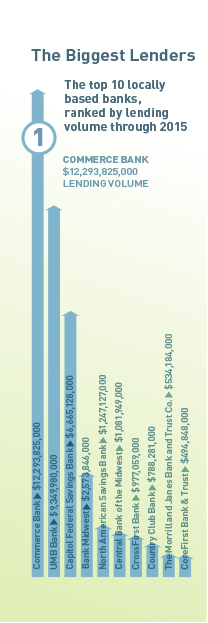

Also of interest were variances in lending strategies. Some banks built their loan operations from scratch. Some expanded from a solid base. Some broadened their lending through strategic acquisition. That paid off for a handful of banks that finished in the Top 10 for both the dollar volume of a loan portfolio, and rate of its growth.

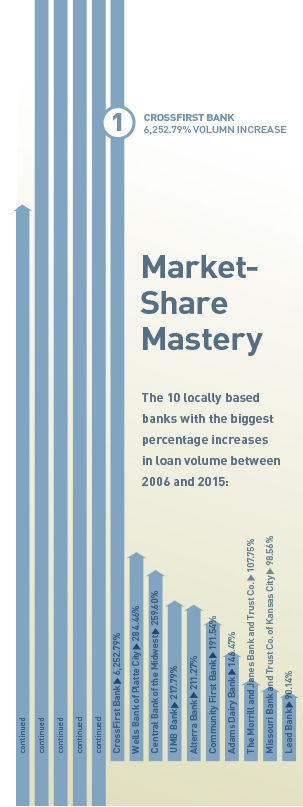

Leawood-based CrossFirst Bank fit the first profile, creating its lending strategy from scratch—the bank didn’t even exist in the first year of the review period—and still went from zero to nearly $1 billion in loan volume. Century-old UMB, by contrast, took a solid base of diversified lending, plumbed new categories and expanded others, and found a formula for success. And Central Bank of the Midwest successfully pursued a series of strategic acquisitions that not only absorbed healthy banks, but banks with loan portfolios that complemented and expanded an existing set of lending strengths.

“When the bank first started, we were probably a little more conservative,” said Mike Maddox, CEO at CrossFirst. “After a couple of years, we evolved and really started to turn to the mid-market commercial banking market; we have a very balanced portfolio between real estate and C&I lending.” Along the way, the bank has expanded into other geographic markets, and this fall will be entering the fray in Dallas on its rise to nearly $1 billion in overall lending and in assets.

Growth has come from spotting opportunities and moving quickly. In just the past few years, CrossFirst added an energy portfolio, which now accounts for about 10 percent of its lending. “It’s like a snowball,” Maddox said. “It just gets bigger and bigger, and each time, the growth compounds.” In addition to working primarily with closely held companies, which have been around and have a track record of performance through good times and bad, CrossFirst targets early-stage companies, as well as smaller ones borrowing $2 million or less.

Despite UMB’s long history of conservative lending and administration—it was ranked by Forbes as the best-performing bank in continental U.S. as recently as 2012—the region’s second-biggest bank in terms of assets has grown its loan portfolio in ways that might defy conservative expectations. Its farm lending increased more than 1,314 percent, for example, while loans for 1-4 family residential properties were up even more at 1,982 percent and loans for construction and development rose more than 428 percent. Those lending lines contributed to an overall increase of 217.79 percent on a base that was already huge, and now approaches $9.35 billion.

“If we go back to the end of 2008, obviously we were in very strong financial condition,” said Jim Rine, president of the KC region. “Our credit philosophy served us well during that period.” The bank’s mantra is “right people, right products and the right mix,” and it all came into play as the marketplace was shifting and consolidating.

“In early 2012, we started to expand our commercial real estate offering and that has contributed to some of our growth,” Rine said. The traditional C&I lending line had always been strong, he said, and the bank was able to capitalize on longstanding relationships with area contractors to leverage permanent loans out of a rebound in construction lending.

What the bank saw during the market contraction, he said, was that “during the actual recession, good customers were looking to get out of bad banks.” That presented some strong opportunities not just with new borrowers, but new faces with unusually low credit risk.

For Central Bank of the Midwest, the rise to dual Top 10 status for both volume and growth was a step-and-repeat function. CEO Tom Fitzsimmons said acq-uisitions over the past decade weren’t grounded in just getting bigger, but getting selectively bigger, in ways that broadened the bank’s appeal as a lender.

“I would attribute about 60 percent of that growth to those acquisitions, and about 40 percent, or slightly below, to core internal growth,” he said. “We traditionally have been

a commercial real estate and residential lender from a construction standpoint. But we’re always interested in increasing our C&I lending, and that did factor in,” as did emerging opportunities to serve consumers on the retail side, particularly with vehicle lending.

And the opportunities, he said, seem to keep on coming. “The concern is over the margins, which continue to shrink, and the competition continues to get stronger,” Fitzsimmons said. “Lenders see the low-rate environment as likely to continue for some while, but overall, we think the Kansas City region is very strong.”