HOME | ABOUT US | MEDIA KIT | CONTACT US | INQUIRE

HOME | ABOUT US | MEDIA KIT | CONTACT US | INQUIRE

July 21, 2010, represents a watershed day in U.S. banking history: On that steamy Wednesday morning in Washington D.C., President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act.

Ostensibly, the nation would address the issue of banks that represented potential threats to the economy by virtue of their sheer size—not just too big to fail, but too big to be allowed to fail. The stated intent was to take some of the air out of the tires of the mega-banks, and to ensure that the failure of any one of them wouldn’t trigger another financial-services meltdown like we saw in 2008.

Five years after its implementation, Dodd-Frank has indeed changed the national and regional banking landscape, but not entirely as its promoters said it would. The financial panic of 2008 was grounded in banking fundamentals that exposed many institutions as poor performers, but the new regulatory mandates, industry executives say, fell hardest on small banks. The costs of meeting those requirements are one reason why the nation has 1,400 fewer banks today than it did at the start of 2011.

And along the way, the share of deposits held by the nation’s 10 biggest banks rose from 45 percent in 2010 to 47.15 percent at the end of 2015. That’s right: Even after “Too Big to Fail” was enacted, nearly half the nation’s bank deposits are in the hands of fewer than a dozen banks.

That breadth of change on the banking landscape in Missouri and Kansas can be measured in different ways. An Ingram’s analysis of comprehensive data compiled by the Federal Deposit Insurance Corp. offers some insights into the various ways that the regional banking sector has changed.

Among them:

• As a region, we’ve bucked that national trend in mega-bank domination of the market. The 10 largest banks serving the two-state market, including national giants like US Bank and Bank of America, controlled 44.76 percent of the region’s deposit market share at the start of 2011. But by 2015, that had dipped to a collective 41.18 percent.

• As a region, we have not escaped the consolidation trend. Nationwide, 1,043 mergers occurred from 2011 through 2015. The two-state region saw 69 banks leave the market, as we fell from 698 banks to 628. The U.S., meanwhile, saw only two new banks chartered since 2012—one each in 2013 and 2015, and none in 2012 or 2014.

• Among banks headquartered in this region, 296 based in Missouri survived the five-year period; in Kansas, 273 were still operating at the end of 2015, a two-state total of 569.

• Just under half the banks in the region, 278, had assets above $100 million in 2010; by 2015, that benchmark was achieved by 324 banks. In Kansas, 25 banks made that leap, bringing the statewide total to 133. In Missouri, 21 broke the $100 million barrier, bringing the total for that group to 191. And across the region, nine banks joined the billion-dollar club, up from 20 in 2011.

• The 10 largest banks went from 38.99 percent of all deposits to 42.20. While that was just a shift of 3.21 percentage points in share, it was a gain of 8.23 percent in collective market share.

The challenges facing smaller banks are also reflected in various figures, particularly in revenues and earnings:

• Only one of the 221 regional banks with assets above $100 million in 2015 posted lower revenues than they saw in 2011, compared to 22 banks below that asset threshold. In other words, 95.95 percent of all banks had higher revenues in 2015 than in 2010, with smaller banks accounting for nearly all of the decline.

• And of the 10 smallest banks by assets, half finished with lower revenues in 2015 than they posted in 2010.

• Perhaps most telling was the difference in the average increase in net income between the two bank cohorts: For those with at least $100 million in assets in 2010, net income rose 146.1 percent by 2015. For those below that level, the figure was 109.4 percent.

But the statistics also offer indications that, among the smaller community banks in the region, those that have survived have taken the worst of the regulatory burden, stabilized, and are moving forward:

• Out of 276 banks with assets of more than $100 million in 2010, average growth in that metric was 29.09 percent by 2015. A bit surprisingly smaller banks saw a growth rate that was slightly higher, 29.11 percent.

• And among those with assets of less than $100 million, the past three years have seen the difference between return on assets for their group cut in half compare to larger banks, suggesting that smaller banks still in operation have weathered the worst.

The FDIC data is replete with story lines of banks that have jumped into a new regulatory environment and found ways not to just survive, but prosper, sometimes in astonishing fashion.

One of those was the smallest bank in the two-state region the year Dodd-Frank was signed: TriCentury Bank, based in the north-central Kansas burg of Simpson, population 86. That year, it had just shy of $4.6 million in assets—little more than a rounding error at Commerce Bank, the bi-state behemoth that had $18.34 billion that same year.

With a population that had fallen by 28 percent since the 2000 census, the writing was on the wall: TriCentury had to change, or die. Travis Hicks, a veteran of the Kansas City banking scene, acquired an ownership stake in 2014 and the bank re-chartered in Johnson County by buying locations in Spring Hill and DeSoto from Equity Bank.

Just a year later, TriCentury’s asset base stood at $54.4 million—an increase of 1,149 percent over 2010. This, mind you, in a county that represents perhaps the most competitive banking venue in the state. How did they pull that off?

“With lots of hard work,” says Hicks, the bank’s president. “Building new relationships and hard work. We have to go out there and beat the bushes and provide the service to get it. Business people want to deal with knowledgeable bankers and to get decisions quickly, and that’s what we’ve done.” It also helped, he said, to steer away from mortgage lending and the additional regulatory challenges that come with it.

TriCentury, in some ways, represents the dichotomy at work in Kansas banking. “A lot of small towns in Kansas are struggling because of the lack of economic activity there,” Hicks said. “The population base is moving out, so for us, the strategy was to bring that charter to the Kansas City market and grow from there.”

Not every small bank in the state can make that tactic work, of course, but the fact that his bank can reflect the current realities of the small-banking business: The Simpson office is closed, but the bank forges on. “Community banks will always be needed,” Hicks says. “We have the ability to provide services and build relationships, and those are competitive advantages for a bank.”

On the other end of the spectrum is UMB, ranking second only to Commerce among local banks in assets. In that five-year period, UMB added nearly $8.2 billion to its asset base, accounting for more than 28 percent of the combined asset growth among its Top 10 peers.

Mike Hagedorn, UMB’s chief executive officer, cited three reasons for that: new lending verticals in agriculture, real estate, health care and aviation, which he calls “business mixes where UMB has a right to play.” Second was geographic expansion, with branch operations that have topped the billion-dollar mark in St. Louis and Denver, plus significant growth in Phoenix, Dallas and Fort Worth. And third, acquisitions of solid operations.

“We have pro-actively identified banks, partners and good operations that survived 2008, which was the litmus test of all stress tests,” Hagedorn said. “We hear a lot of times in the press about a flight to quality, and I think after 2008, that was clearly going on. But I don’t know how much people really care about that in 2016. For us, growth is really more of a function of the effectiveness of our sales people on the street every single day.”

That, he says, along with a “fanatical” approach to ensuring that the bank has the right business model. But is that growth sustainable? “We’re concerned about the economy, the Dow, oil prices—those things generally play a lot into that,” he said. “We’re certainly going to continue to try. We have a 60-62 percent loan-to-deposit ratio, and that’s a lot of dry power to put to work.”

Deposits, he said, “are the raw materials of a bank. We focus on deposit growth more than on looking at assets. But there’s no question that, for the smaller banks, there is some regulatory fatigue, that costs of people and costs for technology are higher than they are comfortable with.”

Max Cook and Chuck Stones are the two people with perhaps the broadest views of banking challenges and opportunities in the region. Cook is president and CEO of the Missouri Bankers Association, and Stones is his counterpart with the Kansas Bankers Association.

Both see signs of hope in the regional community banking sector, but both are acutely aware of continuing challenges therein.

“The reality of it is that compliance costs for all banks post Dodd-Frank have exploded,” Cook says. “Of course, the law of economics always works: The greater the base to spread those costs, the better off you are. So the smaller banks are struggling more so than everybody else.”

Success at that level, he said, had a lot to do with the people running the show at various banks. “There are exceptions to every rule,” Cook said. “There are a lot of great community banks that are nimble and can figure out ways to accommodate all of those requirements that go with them and still do a good job and be profitable for shareholders.”

But based on regional mergers and acquisitions in recent years, he said, nimble will get you only so far: At some level, a bank needs the economy of scale to help disperse those costs. “We’re seeing a little higher number of banks joining forces and trying to reach some critical mass they feel is necessary in their marketplace to do a better job,” Cook said.

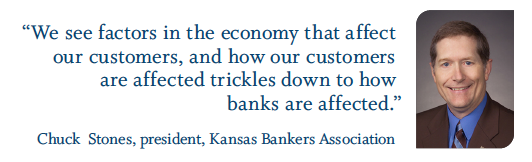

The issue for this region, said Stones, is that banks don’t operate in a vacuum. Many that might have gone under in 2008 were able to get through the crisis by riding the strengths of the agricultural economy. Now that the farm sector is hitting a rough patch—and oil and aviation manufacturing in Kansas, as well, he noted—the concerns fostered by regulation inspire a new level of caution.

“I think banks are a lagging, lagging indicator,” Stones said. “We see factors in the economy that affect our customers, and how our customers are affected trickles down to how banks are affected.”

The challenge going forward, Stones said, is that there’s no indication of an easing in new reporting mandates. “Just from the tenor of what’s going on in D.C., I don’t see a lot of the new regulatory surge slowing down,” he said. “We’ve seen a lot of it, but we’re getting hit by a lot more.”

That suggests a continuation of the consolidation wave that has swept the nation and the region. But in a two-state area fueled by an agricultural economy, can the region stand to go from 570 banks to, say 400? 300? Fewer?

“The answer is, sure, we can,” said Stones. “Does it have an impact on our state and communities and businesses? Yes, I think it does. As we lose more and more of our charters, more and more communities and neighborhoods are served by branches of institutions, not headquarters, and there may be some that don’t know the community as well. There’s always the possibility that there could be some more drop-off.”

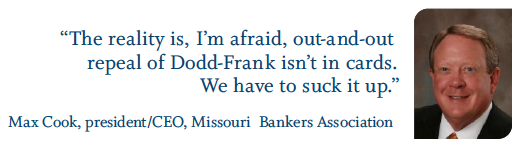

Cook, for his part, says it’s past time for bankers to take the energy spent complaining about regulations and channel it into new strategies for coping, and for growth.

“When the history books are written, this is going to be looked upon as one of the biggest adjustment periods we’ve seen since the Great Depression,” he said. “But there’s always going to be change and movement in markets—population shifts, demogra-phic shifts, cultural shifts.

“I say we have to move forward. Do we have to like it all? No, but we have to accept it. It’s time that, as an industry, we move forward do our best to operate under new rules. We’ll do what we can to tweak, change, maybe even repeal certain aspects of the regulatory environment, but the reality is, I’m afraid, that out-and-out repeal of Dodd-Frank isn’t in the cards.

“We have to suck it up.”