HOME | ABOUT US | MEDIA KIT | CONTACT US | INQUIRE

HOME | ABOUT US | MEDIA KIT | CONTACT US | INQUIRE

Ingram’s 2018 Economic Forecast

If you’re looking for signs that tell you just how good things are right now in the U.S. economy, you don’t have to look very hard—or very far. Among those data points to surface in recent weeks:

All of that came before mid-December, when Congress weighed in with the most extensive rewrite of tax laws in three decades, slashing the corporate income tax rate by more than a third, to 21 percent. And before the holiday shopping season, early indicators of which suggest that a vital piece of broader recovery—consumer spending—was back in force.

So taking all of that in, a reading of the tea leaves suggests a booming 2018, right?

Well … probably. Interviews with prominent economists in the Kansas City region paint a picture of a coming year as one of possibilities, a year fraught with hope, but as 2019 approaches, reason for caution.

Despite the cheery metrics, some indicators are still limping along, said Ernie Goss, an economist who studies the regional economy for Creighton University, and some of those point to potential problems.

“First, the labor-force participation rate remains at 1970s levels,” he said. “Second, annual wage growth remains below 2.6 percent, or only slightly ahead of inflation. Third, the nation’s debt level, at approximately $20 trillion, will push interest rates higher as the economy continues to improve and income tax collections fall due to federal overspending. Fourth, and most troubling, is the slow labor productivity growth. Without an expansion in labor productivity, wage growth will not climb to levels essential for a rising middle-class.”

Diane Dercher of Wealth Manage-ment Advisors in Overland Park sees risks ahead if Trump follows through on major changes in trade policy. “Increased protectionism would be negative for the U.S. economy,” she said. “Increased tariffs would make imported products more expensive for U.S. consumers—they will have less spending power. If other countries retaliate, U.S. exports would weaken leading export dependent business to lay off workers, hurting consumer income.”

Still, a level of optimism abounds, unseen in more than a decade.

“This is about as enthusiastic as economists have been in more than a decade, but it’s our job to find the dark clouds behind every silver lining,” says Chris Kuehl, managing director of Armada Corporate Intelligence. “The worry, amazingly enough, is that we might be growing too fast in the first six months of 2018, setting us up for a fall in the second half.”

Kuehl and his peers recognize positive trends across a broad spectrum of economic indicators. But they also draw on years of experience as investment managers, economic-development consultants and strategic analysts who have made it their job to identify uncharted hazards ahead. And there are always uncharted hazards lurking.

For the U.S. economy in 2018, some of the biggest of those lie overseas. Most prominent among the concerns is the potential for conflict with Vladimir Putin or Xi Jinping, who have made remarkable consolidations of power in Russia and China; the risk of military confrontation over North Korea’s nuclear ambitions; and continuing instability in the economies of some European Union members—the current separatist push in Spain’s Catalan province being but one example.

And yet, the global outlook may be more positive now than in the lifetime of anyone living today. “All 45 countries tracked by the Organization for Economic Cooperation and Develop-ment are growing, the first time in a decade,” Dercher said. And 33 of those show growth accelerating for the first time since 2010, she said. On top of that, “the All Country World Index has now trended higher for close to a year and a half without a 5 percent correction, the longest stretch in ACWI’s 30-year history,” one reason why major countries’ stock markets have outperformed the S&P 500 in 2017, she said.

But there are domestic concerns, as well. Will the increasingly tight labor market choke off business expansion and hiring? Will competition for workers trigger payroll increases and, potentially, trigger inflation? Will the Federal Reserve follow through on promised increases that could take interest rates back over 3 percent for the first time in a decade?

“Things are looking good, but over-

optimism now would be ill-advised, just as extreme pessimism was during the darkest hours of the global financial crisis” a decade ago, says Jamie Battmer, chief economist and lead portfolio manager for Bukaty Companies. “It’s like most everything else—it’s never really as good or as bad as things seem.”

Fuel Sources

If you think of the U.S. economy as a campfire, consider some of the firewood on hand. One of the most under-reported phenomena of the Trump presidency has been his administration’s dismantling of the regulatory framework.

The Washington-based Competitive Enterprise Institute, a libertarian think tank, said last year that it expected the 97,000 pages of the Federal Register to be cut by a third under Trump. Good news for businesses, perhaps, but a possible caution sign for law firms. Even before taking office, Trump vowed to overturn hundreds of regulations his predecessor signed as executive orders on his way out of the White House, and he’s made good on that.

To the extent that continues, smaller companies should feel relief, even if that won’t be immediately clear, said Joe Haslag, a University of Missouri economist who called that development “the thing most in small business’ favor. We have to wait for the data to come in, we’re not going to see what happens in 2017-18 for another year at least. Do people feel unfettered enough to open something they call a business, whether it’s a storefront or basement of house?”

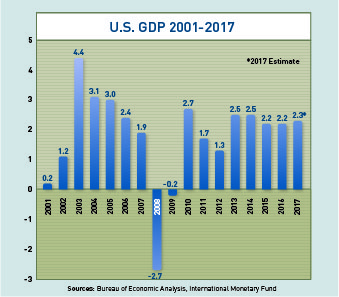

If they do, it’s crucial, because the president’s long-stated goal of sustained GDP growth of 3 percent relies as much, or more, on regulatory reform as on stimulants like corporate tax cuts. And taken as a whole, proponents say, the chemistry between those two developments should produce more growth than the sum of their parts.

Color Kuehl unconvinced. He calls the tax cuts “ill-timed.” “It’s not that they are necessarily a good or bad idea,” he says, “but most economists would agree, this would have been a great plan four or five years ago when the economy was slow, unemployment was high and there was no growth. That’s the ultimate stimulus.” Now, he says, eight years after the Fed and others first urged Congress to do something, it has—just as the economy was already asserting some strength.

U.S. Bank economist Dan Heck-man is keeping a close watch on interest rates, given the Federal Reserve’s indication that three more hikes are likely this year. But anyone with a memory that runs back to the 1980s will have a perspective that puts a quarter-point increase into a larger context—going from 2.4 percent to 3.5 in three or four steps requires incremental bumps that would amount to rounding errors in the early ’80s, an era of 18 percent interest.

“I think rates are still low enough,” Heckman said. “There’s the old saying, three steps and as\ stumble, and what that means is when the Fed raises rates three times, sometimes they over-react and send the economy into recession. I don’t think we see that here; the foundation is pretty strong at this time, so it’s hard to see a recessionary scenario. Perhaps in 2019 or ’20.”

The Business Owner’s Outlook

The challenge for a small business owner sifting through all the macroeconomic analysis and daily metrics of the 24/7 cable news shows is how to read the tea leaves for guidance. Owners can manage capital expenditures, benefit costs and employee head-counts, but factors outside their control—when the Fed will raise rates, and by how much, for example—rarely offer guidance.

Some, says Bill Greiner, chief economic strategist for wealth advisory firm Mariner, can be discerned if owners will “pay attention to delivery times of order rates. If times are being stretched out, that normally leads to a push on the upside of pricing, in many cases.”

A bottleneck on delivery structures can signal higher pricing, which compel one of two choices, neither one pleasant: “Either the ability to pass that along to the customer or take it and swallow a reduction in profit margin,” Greiner said.

Heckman sees credit availability as an issue, especially with rate increases looming. “Small and mid-size businesses should get the financing they need and lock in the current rate, because you may be looking at higher financing costs down the road,” he said.

For Erik Olsen, an economics professor at the University of Missouri-Kan-

sas City, “the biggest threat to small bus-inesses is, and will remain, larger businesses. In an environment of investment and growth, competitive pressures from larger businesses will increase as they look to expand their markets,” he said.

Goss, who also owns a small economic consulting business, says, “my biggest concerns are reckless and unpredictable government regulatory and tax policies.” That includes the possibility that, as the national debt rises relative to GDP, the federal government will seek to increase tax collections.

Under that scenario, he says, “business owners that have successfully saved funds for retirement via IRAs, 401(k) plans, SEP IRAs, etc., could see their withdrawals taxed at a much higher rate, or have their balances subject to a wealth tax (a la France).”

Perhaps the most pressing of emerging threats is labor availability and cost.

“It’s a problem,” said Battmer. Even at Bukaty, he said, “we have seven unfilled positions. It’s a skills gap. We’re not looking for pharmacists or nurse practitioners. That’s a real challenge with the jobless rate dropping as low as it has. We haven’t seen that matriculate into wage growth, because many companies are replacing older workers with younger ones, and inflation hasn’t caught hold—yet. But finding qualified workers is a big issue for a lot of companies.

Typically, reduced unemployment leads to wage growth, said Olsen, and that translates macroeconomic performance into broad-based improvements in income. “But this has not yet been observed in most areas,” he said. “There are a lot of reasons why this is not occurring, and until it does a crucial aspect of economic performance is missing.”

A recent Mariner poll of owners found that only 12 percent say it’s easy to find qualified people, “and that’s indicative of very full labor market,” Greiner said. “To keep good, quality people, many owners have to look at paying up. The day of not giving people a pay increase year after year, those days are probably gone.”